Response

No. In supersession of instructions contained in circular DBOD.No.Leg. BC.44/09.07.005/2005-06 dated November 11, 2005 on No Frill accounts, banks have now been advised to offer a 'Basic Savings Bank Deposit Account' to all their customers vide DBOD.No.Leg.BC.35/09.07.005/20012-13 dated August 10, 2012, which will offer minimum common facilities as stated therein. Banks are required to convert the existing 'no-frills' accounts’ into 'Basic Savings Bank Deposit Accounts'.

Response

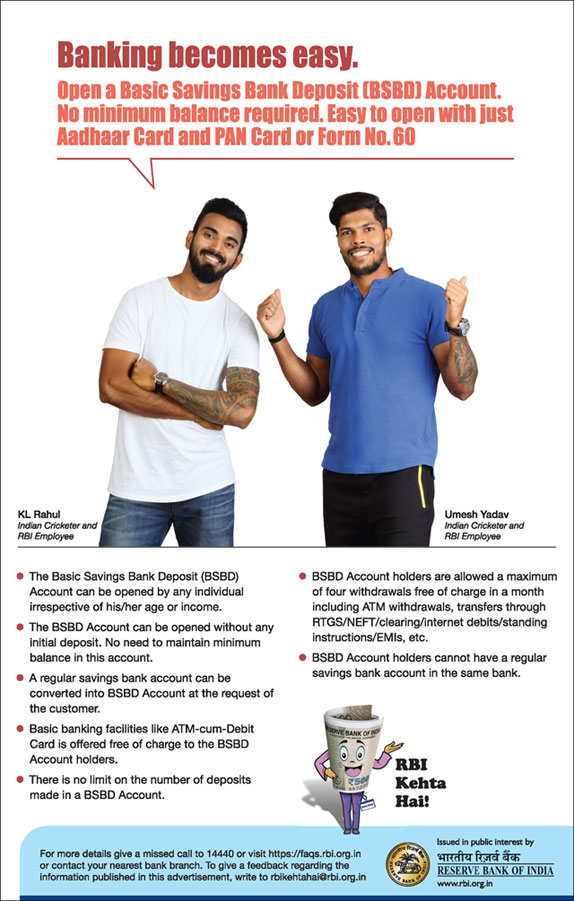

No. An individual is eligible to have only one 'Basic Savings Bank Deposit Account' in one bank.

Response

Holders of 'Basic Savings Bank Deposit Account' will not be eligible for opening any other savings account in that bank. If a customer has any other existing savings account in that bank, he / she will be required to close it within 30 days from the date of opening a 'Basic Savings Bank Deposit Account'.

Response

Yes. One can have Term/Fixed Deposit, Recurring Deposit etc., accounts in the bank where one holds 'Basic Savings Bank Deposit Account'.

Response

No. The 'Basic Savings Bank Deposit Account' should be considered as a normal banking service available to all customers, through branches.

Response

No. Banks are advised not to impose restrictions like age and income criteria of the individual for opening BSBDA.

Response

The aim of introducing 'Basic Savings Bank Deposit Account' is very much part of the efforts of RBI for furthering Financial Inclusion objectives. All the accounts opened earlier as 'no-frills' account vide DBOD Circular dated DBOD.No.Leg.BC.44/09.07.005/2005-06 dated November 11, 2005 should be renamed as BSBDA as per the instructions contained in paragraph 2 of our Circular DBOD. No. Leg. BC. 35/09.07.005/2012-13 dated August 10, 2012 and all the new accounts opened since the issue of our circular DBOD.No.Leg.BC.35 dated August 10, 2012 should be reported under the monthly report of the progress of Financial Inclusion plans submitted by banks to RPCD, CO.

Response

The 'Basic Savings Bank Deposit Account' would be subject to provisions of PML Act and Rules and RBI instructions on Know Your Customer (KYC) / Anti-Money Laundering (AML) for opening of bank accounts issued from time to time. BSBDA can also be opened with simplified KYC norms. However, if BSBDA is opened on the basis of Simplified KYC, the accounts would additionally be treated as “BSBDA-SMALL account” and would be subject to the conditions stipulated for such accounts as indicated in para 2.7 of Master Circular DBOD.AML.BC.No. 11/14.01.001/2012-13 dated July 2, 2012..

Response

No, the BSBDA customer cannot have any other savings bank account in the same bank.. If 'Basic Savings Bank Deposit Account’ is opened on the basis of simplified KYC norms, the account would additionally be treated as a 'Small Account' and would be subject to conditions stipulated for such accounts as indicated in paragraph 2.7 of Master Circular DBOD.AML.BC.No.11/14.01.001/2012-13 dated July 02, 2012 on 'KYC norms / AML standards / Combating of Financing of Terrorism (CFT) / Obligation of banks under PMLA, 2002'.

Response

As notified in terms of Govt of India notification dated December 16, 2010, BSBDA-Small Accounts would be subject to the following conditions:

Response

The services available free in the 'Basic Savings Bank Deposit Account’ will include deposit and withdrawal of cash; receipt / credit of money through electronic payment channels or by means of deposit / collection of cheques at bank branches as well as ATMs.

Response

The services available free in the 'Basic Savings Bank Deposit Account’ will include deposit and withdrawal of cash; receipt / credit of money through electronic payment channels or by means of deposit / collection of cheques at bank branches as well as ATMs.

Response

Yes. However, the decision to allow services beyond the minimum prescribed has been left to the discretion of the banks who can either offer additional services free of charge or evolve requirements including pricing structure for additional value-added services on a reasonable and transparent basis to be applied in a non-discriminatory manner with prior intimation to the customers. Banks are required to put in place a reasonable pricing structure for value added services or prescribe minimum balance requirements which should be displayed prominently and also informed to the customers at the time of account opening. Offering such additional facilities should be non - discretionary, non-discriminatory and transparent to all ‘Basic Savings Bank Deposit Account’ customers. However such accounts enjoying additional facilities will not be treated as BSBDAs.

Response

Yes. Please refer to response to the above query (Query No.13).

However, if the bank does not levy any additional charges and offers more facilities free than those prescribed under BDBDA a/cs without minimum balance then such a/cs can be classified as BSBDA.

Response

No. In BSBDA, banks are required to provide free of charge minimum four withdrawals, through ATMs and other mode including RTGS/NEFT/Clearing/Branch cash withdrawal/transfer/internet debits/standing instructions/EMI etc It is left to the banks to either offer free or charge for additional withdrawal/s. However, in case the banks decide to charge for the additional withdrawal, the pricing structure may be put in place by banks on a reasonable, non-discriminatory and transparent manner by banks.

Response

Banks should offer the ATM Debit Cards free of charge and no Annual fee should be levied on such Cards.

Response

Balance enquiry through ATMs should not be counted in the four withdrawals allowed free of charge at ATMs.

Response

ATM debit cards may be offered at the time of opening BSBDA and issued if the customer requests for the same in writing. Banks need not force ATM debit cards on such customers.

Response

Banks while opening the BSBDA should educate such customers about the ATM Debit Card, ATM PIN and risk associated with it. However, if customer chooses not to have ATM Debit Card banks need not force ATM debit cards on such customers. If, however, customer opts to have an ATM Debit card, banks should provide the same to BSBDA holders through safe delivery channels by adopting the same procedure which they have been adopting for delivery of ATM Debit card and PIN to their other customers.

Response

Yes. BSBDA holders should be offered passbook facility free of charge in line with our instructions contained in Circular DBOD. No. Leg. BC.32 /09.07.005 /2006-07dated October 4, 2006.

Response

While opening the BSBDA customers’ consent in writing be obtained that his existing non-BSBDA Savings Banks accounts will be closed after 30 days of opening BSBDA and banks are free to close such accounts after 30 days.

Response

In BSBDA, banks are required to provide free of charge minimum four withdrawals, including through ATM and other mode. Beyond four withdrawals, it is left to discretion of the banks to either offer free or charge for additional withdrawal/s. However pricing structure may be put in place by banks on a reasonable, non-discretionary, non-discriminatory and transparent manner by banks.

Response

Our instructions contained in circular DBOD.Dir.BC.75/13.03.00/2011-12 dated January 25, 2012 on Deregulation of Savings Bank Deposit Interest Rate, are applicable to deposits held in ‘Basic Savings Bank Deposit Account’.

Response

DPSS. CO.CHD. No. 274/03.01.02/2012-13 dated August 10, 2012

BSBDA does not envisage cheque book facility in the minimum facilities that it should provide to BSBDA customers. They are free to extend any additional facility including cheque book facility free of charge (in which case the account remains BSBDA) or charge for the additional facilities (in which case the account is not BSBDA).

Response

All the existing ‘No-frills’ accounts opened pursuant to guidelines issued vide circular DBOD. No. Leg. BC. 44/09.07.005/2005-06 dated November 11, 2005 and converted into BSBDA in compliance with the guidelines issued in circular DBOD.No.Leg.BC.35/09.07.005/20012-13 dated August 10, 2012 as well as fresh accounts opened under the said circular should be treated as BSBDA. Accounts enjoying additional facilities under the reasonable pricing structure for value added services, exclusively for BSBDA customers should not be treated as BSBDAs.

Response

All the existing “No-Frill” accounts may be treated as BSBDA accounts from the date of the circular i.e., August 10, 2012 and banks may offer the prescribed facilities as per the circular such as issuing ATM card etc., to the existing ‘No-Frill’ account holders as and when the customer approaches the bank. However, for customers opening new accounts after the issue of our circular should be provided with the prescribed facilities immediately on opening of the account.

Response

Yes. Such customers should give their consent in writing and they should be informed of the features and extent of services available in BSBDAs.

Response

RBI instructions/guidelines contained in circular dated August 10, 2012 on BSBDA is applicable to all scheduled commercial banks in India including Foreign Banks having branches in India.